There is a specific type of beginner options trade that follows a very predictable script. Someone with a rocket emoji in their bio says a stock is "about to explode." You buy the call. The stock goes up slightly, but not enough, and not fast enough and the position expires worthless anyway. You discover two things simultaneously: time is a real variable with a dollar value attached to it, and the market has no obligation to confirm your thesis on your schedule.

This guide is about doing something different. Not sexier. Not more cinematic. Just more structurally sound.

Why the Wheel Exists

Most beginners approach options from the buying side. The logic seems intuitive: predict a direction, buy the corresponding option, collect the reward if correct. The problem is that being directionally correct is only one of three conditions required to profit on a long option.

You also need the move to happen fast enough before time decay consumes the position. And far enough past the break-even point formed by the premium you paid. All three conditions, simultaneously. Most of the time, at least one fails.

The Wheel flips this structure. Instead of buying options and racing against time, you sell options and let time work for you. Premium arrives in your account the moment the trade opens. Time passing is no longer the enemy. It is the mechanism.

This is the mental shift that defines the strategy. Not magic. Not a shortcut. Just better alignment between how options actually behave and how a systematic trader can exploit that behavior.

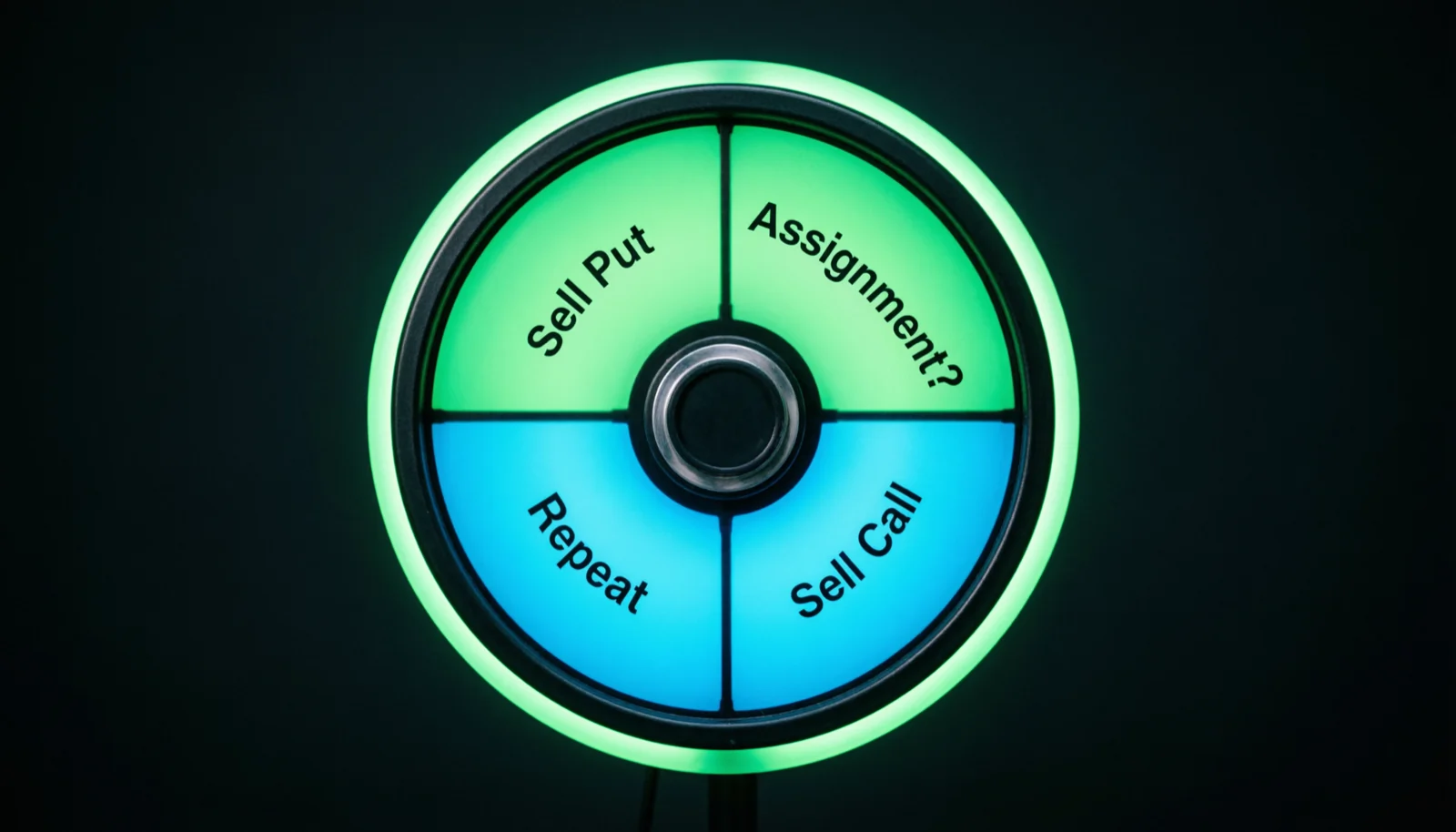

The Loop: How the Wheel Actually Works

The Wheel is a mechanical, repeating cycle with two active phases and a simple decision at each node.

SELL CASH-SECURED PUT

│

├─ Expires worthless → Keep premium → REPEAT

│

└─ Assigned → Own 100 shares

│

└─ SELL COVERED CALL

│

├─ Expires worthless → Keep shares + premium → REPEAT

│

└─ Shares called away → Capital freed → REPEATAt every node, only two things can happen. You always know what they are before the trade opens. That predictability is the entire point of the framework.

The one-sentence definition: You get paid to try to buy a stock at a discount. If you end up buying it, you get paid to try to sell it higher.

Paid to enter. Paid to wait. Paid to exit.

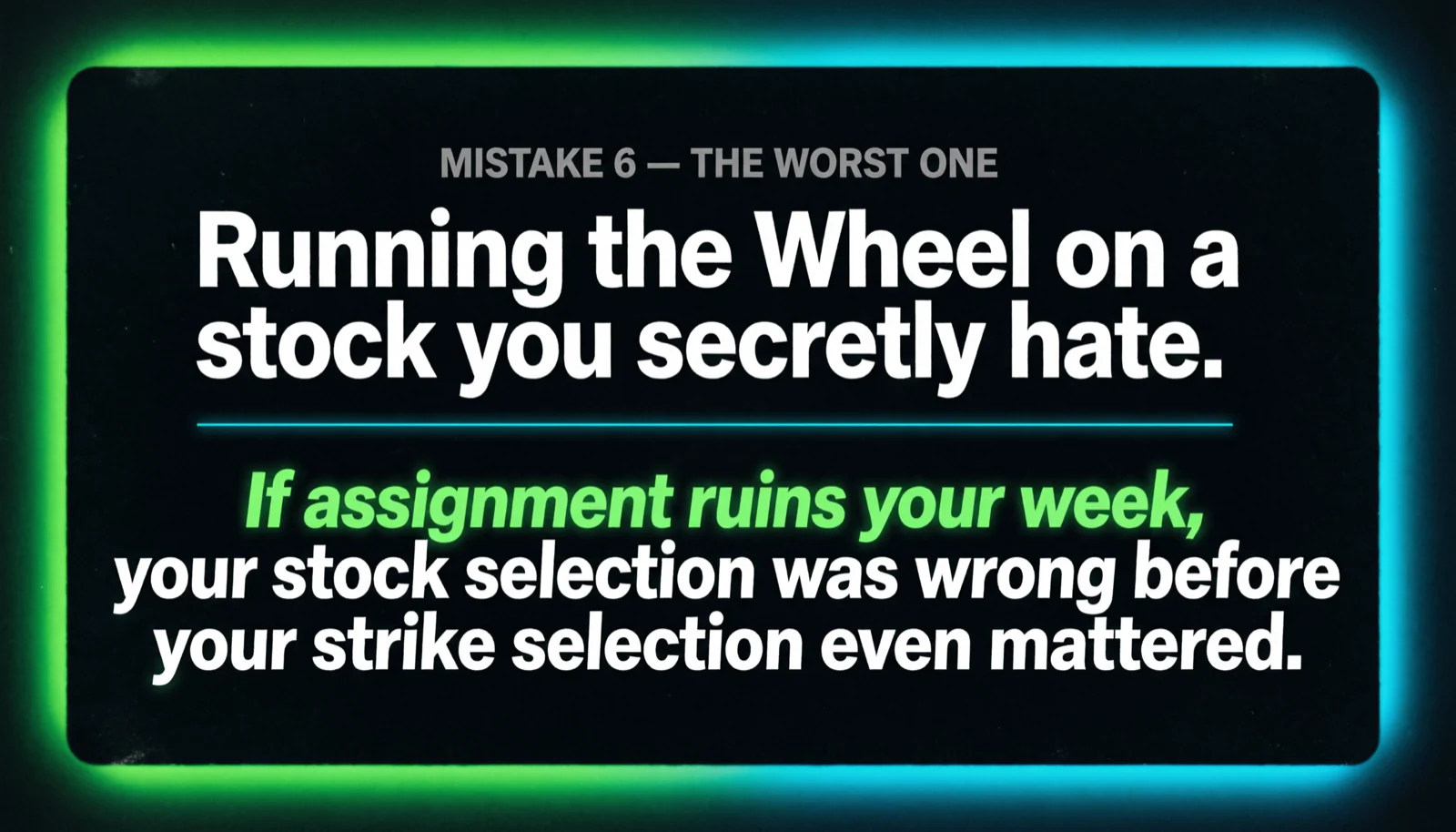

Rule Zero: Stock Selection Comes Before Everything

Before delta. Before strike selection. Before DTE. Before any of the mechanics below. This is the filter that determines whether the Wheel works or fails.

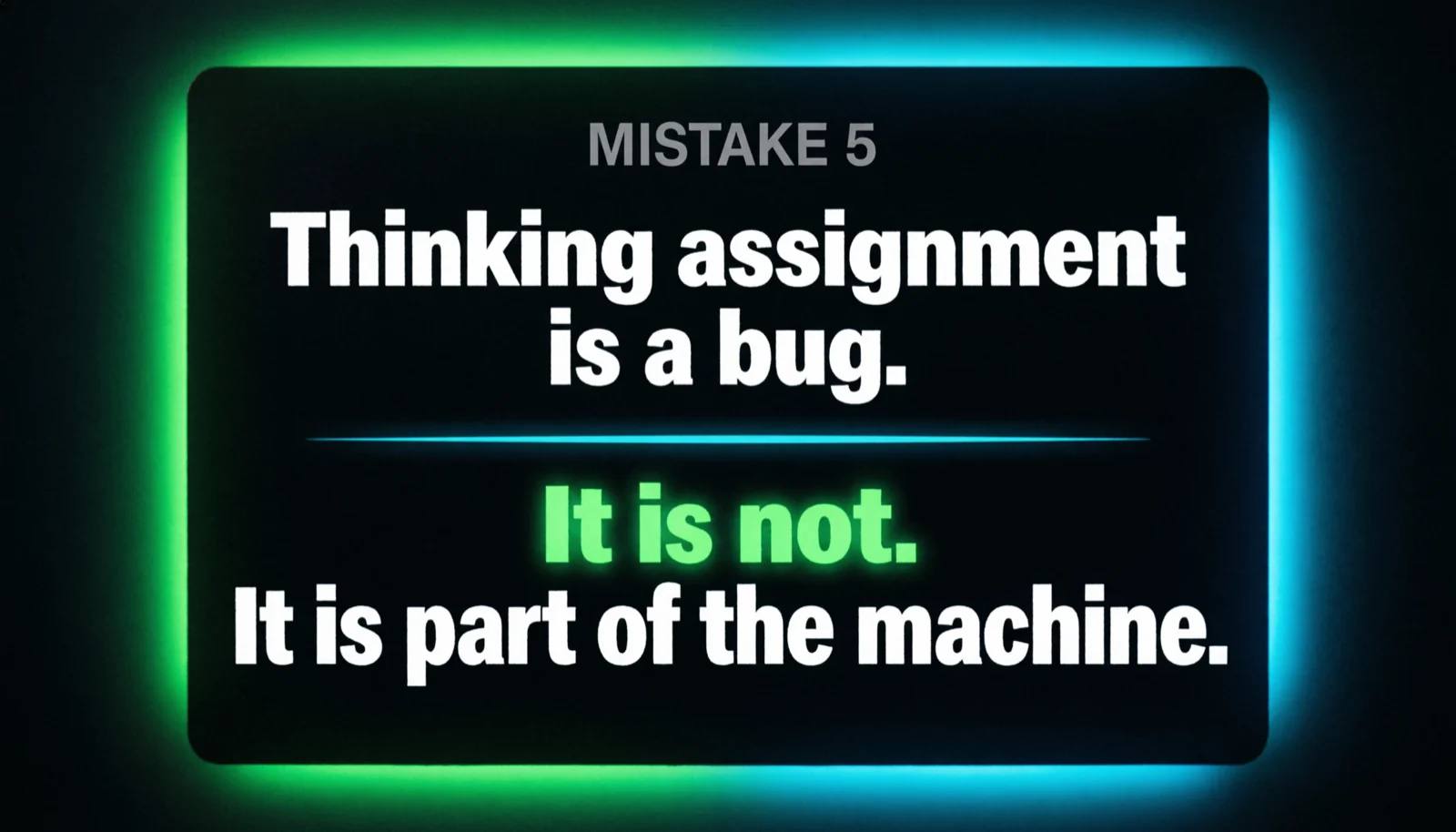

This is not a preference. It is a structural requirement. Assignment is not a bug in the system, and it is not a worst-case scenario you are hoping to avoid. It is a designed, anticipated outcome built into the strategy. The Wheel is specifically constructed around the possibility that you end up holding 100 shares.

If that possibility is unacceptable to you, the trade is wrong before you even open the options chain.

The failure mode looks like this: someone selects a stock because the premium is high, not because they want to own the company. The premium is high for a reason. The market is pricing in elevated risk. They get assigned. Now they own 100 shares of something they never wanted to hold, at a price that is falling, with no conviction to stay in the position.

The Wheel will not save bad stock selection. It will simply make bad stock selection feel more organized.

What "good stock selection" means in practice

- Liquid equity with an active options chain. You want tight bid-ask spreads on the options. Wide spreads silently extract edge on every fill, on both entry and exit.

- Stable enough to own through volatility. Not safe in the sense of zero movement. But not so unstable that a single earnings miss or news event could gap it down 40% overnight.

- A business you'd still respect if you woke up assigned tomorrow. If the idea of holding 100 shares for several weeks or months creates anxiety, the stock is wrong.

Phase 1: The Cash-Secured Put

A cash-secured put means you sell a put option while simultaneously holding enough cash in your account to purchase 100 shares of the underlying if assigned. The cash is the collateral. It is not optional.

One options contract almost always represents 100 shares. This matters enormously when calculating your actual capital commitment. If a stock trades at $50 and you sell one put at a $48 strike, you are committing $4,800 in collateral, not $48.

Choosing Your Strike and Expiration

Days to Expiration (DTE): target 30-45 days.

This range sits in the zone where theta begins accelerating meaningfully. At 30-45 DTE, you are capturing that acceleration without the operational stress of managing weekly contracts that expire every five days.

Delta: target around 0.30, out of the money.

Delta is a probability proxy, not a guarantee. A 0.30 delta put is commonly interpreted as roughly a 30% chance of expiring in the money, meaning roughly a 70% chance it expires worthless and you keep the premium.

What You're Saying When You Sell the Put

I am willing to buy 100 shares of this stock at this strike price, by this expiration date. In exchange, you pay me a premium right now.

That is it. You are getting paid for your willingness to buy the stock at a specific lower price. The premium is yours immediately, regardless of outcome.

The Two Outcomes

Outcome 1: The put expires worthless.

The stock stays above your strike at expiration. The put expires with no value. You keep the premium in full. Your capital was never deployed into shares.

Outcome 2: You get assigned.

The stock falls below your strike at expiration. You are now obligated to purchase 100 shares at the strike price. That is not failure. It is the contract being executed exactly as written.

The Cost Basis: The Number That Controls Everything After Assignment

When you sell a put and collect premium, that premium permanently reduces your effective entry price on the shares: your adjusted cost basis.

Strike price: $50.00 (gross purchase price per share)

Premium collected: $2.00 (= $200 total received on 1 contract)

─────────────────────────────────

Adjusted cost basis: $48.00 per share

Total capital deployed: $4,800 (but $200 already returned = net $4,800 at risk)Every decision you make in Phase 2, especially which covered call strike to sell, must be evaluated against $48.00, not $50.00.

If you sell a covered call below your adjusted cost basis, you are mathematically locking in a realized loss on the cycle, regardless of how much premium that call generates.

Phase 2: The Covered Call

Once assigned, you own 100 shares. You now move to the second phase: selling a covered call against those shares.

A covered call means you sell a call option while owning the underlying shares as collateral. You are selling someone else the right to buy your 100 shares at a specific strike price, by a specific expiration date. In exchange, you collect another premium.

Choosing Your Strike and Expiration

Same defaults as Phase 1: out of the money, around 30-45 DTE, around 0.30 delta.

Critical constraint: The strike must be above your adjusted cost basis.

The Two Outcomes

Outcome A: The covered call expires worthless.

The stock stays below your strike at expiration. The call expires with no value. You keep your 100 shares. You keep the premium. You sell another covered call.

Outcome B: Your shares get called away.

The stock moves above your strike. The call is exercised. Your 100 shares are sold at the strike price. Your capital is freed. Return to Phase 1. That is the Wheel.

Rolling: Management or Avoidance?

Rolling is the practice of closing your current short option before expiration and opening a new one, typically further out in time and sometimes at a different strike.

What rolling actually is: you close the current position at a loss or reduced profit, and simultaneously open a new position that ideally generates enough credit to offset that loss and create a net benefit.

When rolling is legitimate:

- The new position produces a net credit.

- The new strike and expiration genuinely improve the trade's structure.

- The decision is based on trade logic, not the desire to avoid booking a loss.

When rolling is just paperwork:

- You are rolling because the stock moved against you and you are not ready to accept the trade changed.

- You are extending duration only to sound like you are managing the position.

- There is no net credit and you are paying to extend the commitment.

The Six Mistakes That Break Beginner Wheels

These are not rare edge cases. They are the standard failure modes, roughly in the order of how quietly they destroy accounts.

What the Wheel Does Not Do

The Wheel is not a hedge. Premium income from selling options does not protect you from a significant decline in the underlying stock. If your $50 stock drops to $30, the option premium softens the blow slightly, but the stock was always the primary risk.

The Wheel does not generate infinite yield. Realistic premium is bounded by implied volatility, strike selection, and time.

The Wheel does not remove the emotional component of trading. It structures it.

The Risk That Doesn't Get Talked About Enough

If you pick a structurally weak company, the Wheel can become a very systematic way to keep buying a falling asset. The strategy has no built-in exit mechanism for that scenario. You need one externally: a maximum loss threshold, a stop rule, or a fundamental re-evaluation.

Premium collection is not a substitute for an exit strategy.

A Framework, Not a Shortcut

The Wheel works as a beginner framework because it forces you to learn the things that actually matter. You cannot run it without understanding collateral requirements. You cannot run it profitably without tracking cost basis. You cannot survive it without stock conviction. You cannot optimize it without understanding time decay.

It is not a strategy that makes you feel like a genius every twelve minutes. It is a strategy that teaches you how options actually work while giving you a systematic loop to operate inside.

The log is open. The math is public. The premium is waiting.